Can You Sell Your House to Settle a Debt in Kentucky?

Debt collectors calling daily while your mortgage falls behind feels like drowning in quicksand. Your home equity sits untapped while creditors threaten legal action and foreclosure looms closer. Financial stress mounts as options seem to disappear, leaving you feeling trapped and helpless. Selling your Kentucky house can eliminate debts quickly and give you a fresh start.

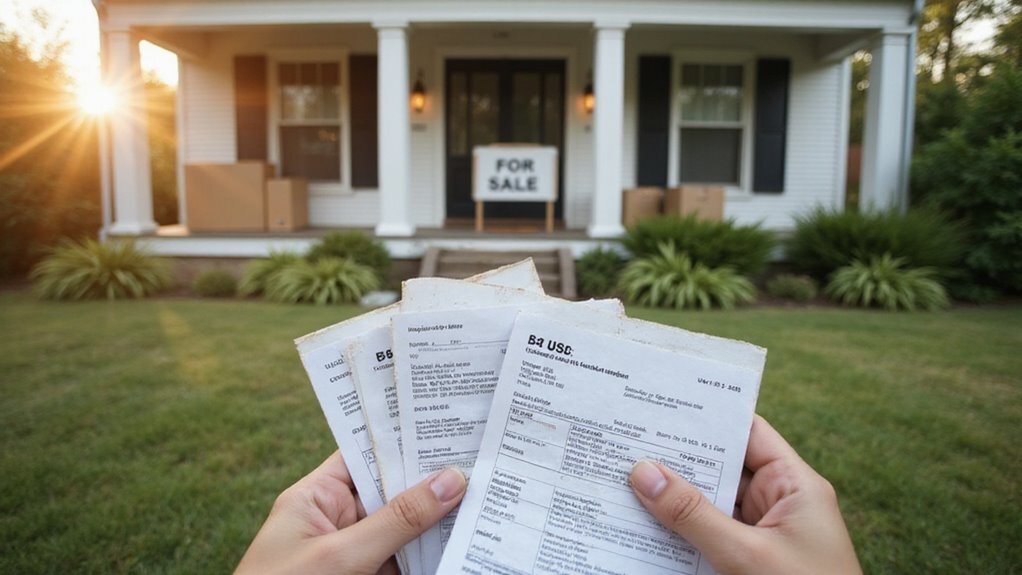

Selling your house to settle debt in Kentucky is legal and often necessary. You can use sale proceeds to pay off mortgages, liens, and judgments. The process typically takes 30-60 days with proper preparation and realistic pricing.

In this guide I will explore everything related to selling a house to settle debt in Kentucky.

Key Takeaways

- Selling your Kentucky home can quickly settle secured debts like mortgages, liens, and overdue taxes.

- Ensure full disclosure of liens and debts to buyers and lenders before selling.

- Calculate home equity and prioritize paying off debts from the sale proceeds.

- Consider legal and tax implications, including capital gains and forgiven debt taxes.

- Act swiftly by preparing the home for sale and exploring cash or quick-sale options to avoid foreclosure.

Can Selling Your House Settle Debts Effectively?

Yes, selling your house can effectively settle debts if you have enough equity. This strategy works best when your home’s value exceeds what you owe.

Property sales provide immediate funds to clear secured debts and liens. You can avoid foreclosure and eliminate mortgage arrears quickly. However, you must address outstanding balances first from sale proceeds.

Kentucky law permits this debt resolution method.

Be aware that short sales require lender approval and may trigger tax implications. Act quickly to prevent your financial situation from deteriorating further.

“Brian with Ky Sell Now couldn’t have been any better to deal with. The offer was reasonable, they did what they said they would do, and did it when they said they would do it. Terms were good and they were flexible meeting our terms and needs.“

David Weinberg

What Are the Types of Debts That Lead to Home Sales?

Debt can force you to sell your home quickly, especially if you’re behind on your mortgage or facing foreclosure.

Unpaid tax liens, government debts, and large credit card balances can also lead to forced sales or court actions.

Recognizing which debts threaten your home is vital to acting fast and protecting your interests.

Mortgage Arrears and Foreclosure Risk

Mortgage arrears occur when you miss payments and fall behind on your home loan. Your lender may start foreclosure proceedings if the debt remains unpaid. This legal process can result in losing your property.

However, you have options to prevent foreclosure. Kentucky law allows mortgage modifications, repayment plans, and deed in lieu arrangements.

Contact your lender immediately when you miss a payment. Early communication often leads to better solutions and protects your home from forced sale.

Tax Liens and Government Debts

Unpaid taxes and government debts can result in liens against your property. These liens give authorities the right to collect what you owe. Your home can’t be sold or transferred until the debt is cleared.

The government may file liens for unpaid income taxes, property taxes, or estate debts. Time is critical when dealing with these issues.

Prompt action prevents forced sales and protects your ownership. Settle outstanding debts quickly to maintain control of your property and avoid escalating consequences.

Credit Card and Unsecured Debt Accumulation

Credit card balances and personal loans can threaten your ability to keep your home. These unsecured debts may lead creditors to pursue court judgments against you. High debt levels often force homeowners to sell their properties for relief.

You should contact your creditors immediately to discuss payment options. Many creditors will negotiate reduced payments or settlements to avoid legal action.

Early communication protects your credit score and prevents liens on your property. Additionally, exploring debt consolidation might help you avoid selling your home altogether.

Medical Bills and Emergency Expenses

Medical bills and emergency expenses force many homeowners to sell quickly. These costs create immediate financial pressure that regular income can’t cover. Hospital stays can cost $10,000 to $50,000 or more, pushing families into debt.

As a result, mortgage payments fall behind while medical liens accumulate against your property. Foreclosure becomes a real threat within months of missed payments.

Selling your house provides funds to settle debts and prevent credit damage. This decision protects your family’s financial future and offers a fresh start.

Divorce Settlements and Property Division

Divorce often requires selling the marital home to divide assets fairly. The proceeds help settle shared debts and allow both parties to move forward financially.

You must pay off mortgages and liens before completing the sale. Hidden debts create legal problems and slow the process. Full disclosure protects you from future disputes.

Even if you owe more than the home’s value, closing requires debt payment. Quick, honest action ensures debts get covered and protects everyone’s interests during this difficult transition.

How to Sell Your Home to Settle Debt?

You need to act fast—start by assessing your debt and understanding your home’s current market value. Then, consult with financial and legal experts to investigate your best options.

Finally, prepare your property for a quick sale, whether through listing or selling directly to cash buyers.

Evaluating Your Current Debt Situation

Start by listing every debt you owe. Include mortgages, court judgments, liens, and credit card balances. This complete picture shows what needs attention first.

Next, determine which debts attach to your home. Secured debts like mortgages and liens must be paid from sale proceeds. Calculate your home equity by subtracting total debts from your property’s current market value.

Consider debt relief programs if selling won’t cover everything. Understanding your complete financial position helps you choose the best path forward.

Determining Your Home’s Market Value

Your home’s market value depends on what buyers will pay right now in your local area. Recent sales of similar homes establish the baseline price range. The condition of your property matters significantly. Well-maintained homes consistently sell for more money than those needing repairs.

Location plays a critical role in determining value. Desirable neighborhoods command higher prices regardless of other factors. Current market conditions also influence your final sale price. A seller’s market benefits you, while a buyer’s market may require price adjustments.

Consulting with Financial and Legal Advisors

Yes, consult financial and legal advisors before selling your home to settle debts. They protect your interests and prevent costly errors during the sale process.

A financial advisor reviews your debt obligations and calculates what you’ll owe after closing. They identify liens or judgments that must be paid from sale proceeds.

Legal counsel ensures all settlement documents comply with state requirements. Your attorney can explore alternatives if you owe more than your home’s value.

Options include short sales, bankruptcy filing, or deed in lieu arrangements. These professionals work together to structure a sale that satisfies creditors while protecting your legal rights.

Preparing Your Property for a Quick Sale

Prepare your property to attract buyers fast and close the deal quickly. Clean every room and remove clutter to showcase the space.

Buyers need to imagine their own lives in your home, so pack away personal photos and items. Focus on small repairs that make a big impact. Fix leaky faucets, patch wall holes, and freshen paint where needed.

These updates don’t require major investment but boost appeal significantly. Price your home competitively based on current market conditions to avoid lengthy delays and mounting costs.

Listing vs. Direct Sale to Cash Buyers

A direct cash sale closes faster than a traditional listing. You can settle your debts in as little as 7 to 14 days with a cash buyer.

Traditional listings take 30 to 60 days or longer due to inspections and financing delays.

Cash buyers purchase homes as-is, so you skip costly repairs. You also avoid realtor commissions that typically cost 5% to 6% of the sale price.

This approach works best when you need immediate debt relief without complications.

“Brian was so easy to work with. They were quick and efficient. After several months of working with another buyer without closing the deal, we are thankful to have found him. We were able to get a deal done and finalized in just a matter of weeks! I would recommend Kentucky Sell Now to anyone.”

What Are the Legal Considerations You Should Know?

You must understand your legal rights and obligations before selling your home to pay debt. All liens require full disclosure to potential buyers. Secured debts get paid first from your sale proceeds. Kentucky law provides specific protections during this process.

You have rights to notice and redemption in foreclosure cases. Court approval may be necessary for certain creditor settlements. However, forced sales through court-ordered liens remain uncommon.

Consider alternatives before proceeding with a sale. Loan modifications or bankruptcy might better serve your situation. Each option carries different legal implications for your financial future.

What Are the Tax Implications of Selling Your Home for Debt?

Tax Implications of Selling Your Home for Debt You may owe taxes on forgiven debt and capital gains. The IRS treats cancelled debt as taxable income in most cases.

Forgiven debt over $600 typically counts as income. Your lender will send you a 1099-C form to report this amount.

Capital gains taxes apply if your profit exceeds exclusion limits. However, you can exclude up to $250,000 ($500,000 for married couples) if you lived in the home for two of the last five years. Consult a tax professional to calculate your specific liability.

What Are the Alternative Options to Consider?

If you’re facing debt and risk losing your home, don’t wait—explore all your options now. You might qualify for debt consolidation, refinancing, or a loan modification to keep your house.

Alternatively, consider bankruptcy, a short sale, or a deed in lieu to protect your interests and avoid foreclosure.

Debt Consolidation and Refinancing

Debt consolidation combines multiple debts into one payment with a lower interest rate. Refinancing replaces your current loan with a new one, often with better terms. Both strategies can reduce monthly payments and simplify your finances.

Debt consolidation works best when you have good credit and steady income. Refinancing requires home equity and solid credit scores. However, these aren’t your only options when facing financial pressure.

Alternative solutions include negotiating with creditors or seeking government assistance.

Chapter 13 bankruptcy can halt foreclosure proceedings immediately. Short sales and deeds in lieu offer ways to avoid foreclosure entirely.

Loan Modification Programs

Loan modification programs change your existing mortgage terms to lower your monthly payments. They help you avoid foreclosure when financial hardship makes payments difficult.

Your lender may reduce your interest rate, extend your loan term, or forgive part of your principal balance. These changes make payments more affordable.

As a result, you can stay in your home while recovering financially. Contact your lender immediately if you’re struggling with payments. Most lenders offer hardship programs for qualifying homeowners. Quick action increases your chances of approval and prevents foreclosure proceedings.

Bankruptcy Protection Possibilities

Yes, bankruptcy can stop foreclosure and protect your home. Chapter 13 bankruptcy halts foreclosure proceedings immediately and lets you catch up on missed payments over three to five years.

You have other options beyond bankruptcy. Loan modifications can lower your monthly payments. Deed in lieu arrangements let you transfer property ownership to avoid foreclosure damage.

Creditor negotiations may reduce what you owe. Act now rather than waiting. Quick action preserves more options and protects your financial future.

Short Sale Arrangements

A short sale lets you sell your home for less than you owe on your mortgage. Your lender must approve the sale before you proceed. This option helps you avoid foreclosure and protects your credit score from severe damage.

Lenders usually prefer short sales because they cost less than foreclosure. You can resolve your debt and stop legal action against you. Contact your lender immediately to discuss if you qualify for a short sale.

Deed in Lieu of Foreclosure

A deed in lieu of foreclosure lets you transfer your home’s title directly to your lender. This option helps you avoid a lengthy foreclosure process. You must prove financial hardship to qualify.

Your property title needs to be clear of other liens. The lender reviews your situation before accepting the deed. This choice affects your credit score negatively.

You may owe taxes on forgiven debt. However, it resolves your mortgage obligation faster than foreclosure.

How Fast Can You Sell and Settle Your Debt?

You can settle debt through a home sale in as little as 7 to 30 days with the right approach.

Home auctions typically close within days, making them ideal for urgent situations. Cash buyers also speed up the timeline significantly.

However, certain factors may cause delays. Lenders must approve short sales, which can take weeks or months.

Existing liens or court judgments require resolution before closing. Choose your sale method wisely and maintain clear communication with all parties to ensure the fastest possible outcome.

Get Debt Relief Today: Contact Kentucky Sell Now for a Quick Cash Offer

Kentucky Sell Now provides fast cash offers to help you resolve debt quickly. We buy houses directly, which means you avoid the foreclosure process entirely. You receive payment fast and can settle outstanding debts without waiting.

Our process eliminates repairs, showings, and lengthy negotiations. You can close in as little as 7 days. This approach protects your credit score from further damage. More importantly, you regain control of your financial situation immediately. Contact us today for a no-obligation cash offer on your property.

Can I sell my house in Kentucky to pay off debt?

Yes, you can sell your house to pay off personal or financial debts, including credit cards or loans.

Do I need to pay off all debts before selling my home?

No, but any mortgage or lien on the property must be settled from the sale proceeds at closing.

How fast can I sell my house in Kentucky for debt relief?

Cash buyers or investors can close within 7–14 days, while traditional sales may take 30–60 days.

Will selling my house affect my credit score?

Selling doesn’t hurt credit directly, but paying off debts with sale proceeds can help improve your credit.

Can I sell a house in foreclosure to pay off debt?

Yes, if sold before the foreclosure auction, you can use the sale to pay off or reduce your debt.

Sell Your House Fast in Louisville 💰

We buy houses in Louisville As-Is! No Hidden Fees or Real Estate Commissions. Sell Your House in Louisville And Close On The Date Of Your Choice. Simply Fill Out The Form, or call (502) 610-0070 today!